Probably The Best Series On The New Deal (by Selgin)

George Selgin published recently what is probably the best article on the New Deal and he dedicated an entire series of articles in which he questioned the arguments in defense of the New Deal.

Selgin starts to discuss the unemployment estimates during the relevant period (1929-1940) provided by Lebergott (the standard BLS measure) and Darby, the latter showing a lower rate during the 1930s. This is because Darby counted the persons enrolled in the New Deal relief programs as employed. However it was found that those workers wouldn't find any gainful employment elsewhere in the labor market. It is indeed fair to count them as unemployed, as the BLS measure considered them.

Recovery With High Unemployment

A good, better measure of the speed of recovery is the time it takes for output to return to its pre-crisis trend line, which however didn't happen until 1942. The fact that unemployment was persistently high is a big tell that the progress of actual output lagged behind its potential output. Labor, machines and other inputs were left idle. And so did the capital stock, left unchanged.

Yet, output recovered, despite the depression, but only because of improvements in total factor productivity (TFP), as Field puts out :

Since private sector input growth was effectively absent, all of the growth in output was on account of TFP advance. And since there was virtually no capital deepening, almost all of the growth in output per hour (labour productivity) can also be attributed to TFP growth.

Selgin also told us that, by 1937 the U.S.' index of industrial production was still below its 1929 level, with low growth in spurts, contrasting the indexes of several other European nations with steady growth. Those European countries eventually surpassed their pre-depression levels. France alone lagged even further behind than the U.S. Furthermore, the growth in per-capita income in the U.S. was also among the worst of the bunch.

One way to achieve recovery faster is to allow prices to fall as demand falls during the depression. If policies prevent prices from falling, the situation will worsen. A defensive stance on falling price is detailed in his book, Less Than Zero. As Selgin argued :

It follows that the more completely prices respond to fallen spending, the less sales will suffer. Because falling prices, besides preventing inventories from accumulating, also mean falling input costs, production may also be revived.

Fiscal Stimulus Myth

Despite the New Deal, contrary to the statement that the fiscal stimulus brought the depression to an end, such spending wasn't sufficient. While Roosevelt spent twice as much as Hoover's previous administration, there were enough taxes to maintain small deficits. Yet Roosevelt tolerated massive relief spending, and any deficits that went with it, the reason wasn't because he believed in the "fiscal stimulus" policies as no one in the government at that time trusted these policies, but because he didn't want people going hungry.

A popular take on the recovery is based on Christina Romer's studies, which conclude that such recovery was due to monetary expansion. Selgin explains that we ought to understand the cause of that money growth.

The most important of these causes consisted of growth in the size of the Fed's balance sheet. As that grew, so did the sum of bank reserves and the public's holdings of Federal Reserve notes. The size of the Fed's balance sheet in turn depended on the amount of gold (or "gold certificates") that came its way, and also on the nominal value of commercial paper ("bills") and Treasury securities the Fed acquired through its lending and open-market operations. The other source of changes to the money stock consisted of changes in the ratio of the total money stock to the quantity of Fed assets, which itself depended mainly on what ratio of reserves to deposits banks wished or were required to maintain.

As the following FRED chart shows, the rapid money growth between 1933 and 1937 was entirely due to growth in the Fed's gold holdings :

Since the bank deposits increased over time, the blue line increased less than the red line. The Fed's bill and security holdings remained constant, as shown by the purple line. The underlying story is that while the Fed let its balance sheet grow in response to gold inflows, it didn't encourage money growth.

Selgin tells us that the Fed officials were afraid of inflation, since banks had been storing-up excess reserves, they feared that a revival of bank lending might lead to excessive money growth. The Treasury decided to offset gold inflows.

Furthermore, it seems the New Deal played a major role too. The 1932 Glass-Steagall Act allowed the Fed to issue Federal Reserve Notes backed by Treasury securities instead of gold. The Emergency Banking Act of 1933 in turn allowed the Fed's holdings of notes, bills of exchange and bankers' acceptances to be eligible as collateral for the Federal Reserve Notes. The Fed could indeed manipulate bank reserves independently of its gold holdings. But Selgin argued that the Fed wasn't really independent, its monetary policy being under the administration's control.

Monetary Policy

Two other New Deal measures strengthened the administration's control upon monetary policy. First, the Gold Reserve Act of 1934 ordered the Americans to surrender their monetary gold holdings to the Fed in April 1933. The Fed also had to transfer its gold to the U.S. Treasury in exchange for Treasury "gold certificates". Furthermore, the dollar's gold value was altered by proclamation, raising its official price from $20.67 per ounce to $35 per ounce. And since the "gold profit" from the devaluation went not to the Fed but to the Treasury, growth in money stock rests in the Treasury's power. The Second measure comes in the form of the Banking Act of 1935 drafted by Marriner Eccles appointed by Roosevelt as the Fed's new governor. This new law also allowed him to set Fed bank discount rates and reserve requirements.

But discussing depression and monetary policies without describing their banking system wouldn't be fair. As Selgin argued in his book, The Theory of Free Banking, a bank branching system is crucial to maintain stability. And it appeared in the U.S. that branching was prohibited in many states or allowed on a limited basis. The U.S. adopted the "unit banking" system. Instead of conducting business at branches set up in multiple places, the unit banking did so from its headquarters. Thus, the combination of unit banking laws and low regulatory capital requirements had resulted in a banking system consisting mainly of large numbers of very small banks. That was ultimately the reason as to why those banks were so vulnerable to bank panics, like those of 1884, 1893, and 1907. After 1907, WWI encouraged the creation of even more weak banks, no less vulnerable to shocks.

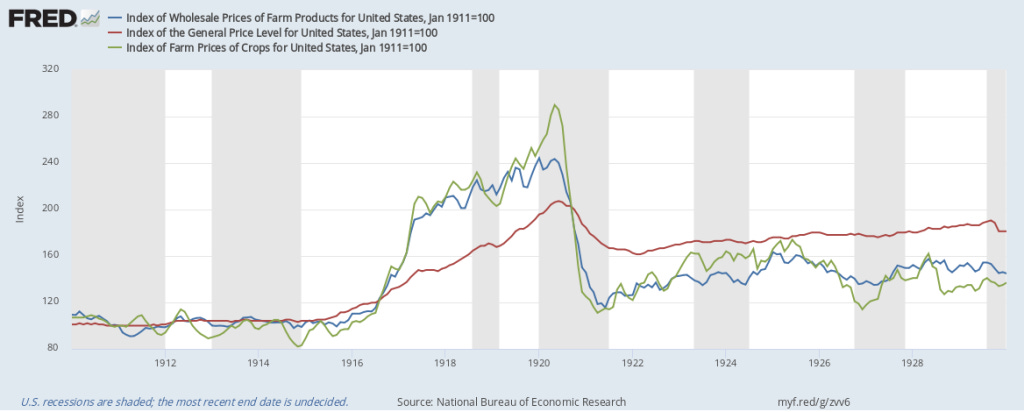

In fact, WWI contributed to a larger degree to bank failures. According to Selgin :

Because the war shut-down many European farms, and troops needed to be fed, crop and livestock prices rose sharply, encouraging U.S. farmers and ranchers to extend their acreage. Then, when the U.S. entered the war, the Agricultural Extension service egged farmers on further with a vigorous campaign aimed at getting them to contribute to the war effort by farming more intensively with the help of tractors and new methods of pest and weed control. More new banks popped up in turn to finance farmers' purchases of land and tractors and other inputs using credit secured by mortgages. Between them, subsidized deposit insurance and the WWI farm boom caused the number of banks to more than double, from 12,427 in 1900 to 30,291 by 1920. Bank lending to farmers itself doubled between the start of the War and 1920.

As Austrian economics understands this behaviour quite well, when the main factor causing the economic boost stops being effective, such a process now has to be reversed. So, after the war, crop prices fell as sharply as they had risen during it, which in turn caused a farm crisis affecting many farmers as well as banks financing them during the war.

Why Everyone Panicked

Yet an external factor paved the way to even more banking troubles. The Bank of England's decision to suspend gold payments caused European central banks to withdraw gold from the United States to bolster their own reserves. This effect in turn frightened American depositors in a way that they started to hold gold themselves, resulting in many more bank failures. At that time, Hoover's counter-measures in the form of an anti-hoarding campaign helped to mitigate the effect of that panic. Also, Hoover during his 1932 campaign speech publicly admitted the country was close to defaulting on its gold payment. This overall seemed enough to instill fear and distrust in people's minds.

Furthermore, imposing bank holidays further weakened people's trust in the banking system. Commercial bankers were reluctant to declare a bank holiday because it damages their reputation. Yet, the governor of Michigan, Comstock, declared a bank holiday in Detroit to save banks due to a collapse in automobile sales. But depositors in other states feared their governor would follow the same example and they started withdrawing their money. It wasn't over yet.

Another factor precipitated the national bank holiday. The conviction that the gold standard would soon come to an end owing to restrictions on gold holdings and expectations of devaluation. Soon, a run on the dollar happened, a third of which was presented to the Fed for payment in gold. Before long the Federal Reserve Bank of New York decided to suspend its gold-reserve requirement. But while New York banks were actually well-prepared to withstand a run, they were asked to declare a bank holiday to hide the information from the public that the Fed was having problems. Officials at the other Fed banks began urging the governors of other states to follow the same procedure. At the time Roosevelt took office, most banks in the country temporarily closed. Selgin shared data on the U.S. gold reserve, and it appeared that the U.S. held a huge amount of gold, enough to withstand a run.

An interesting fact has been reported by the historian Fuller, who stated that after Michigan's crisis, the public remained calm and didn't rush to their banks. The wave of fear originated from bankers and state politicians who reacted not to actual depositor runs but to each other's anxiety about what might happen. The more banks were to close the more the remaining banks feared of not having access or losing correspondent balances, which would further encourage their governors to declare holiday as well. As holidays and restrictions multiplied, bank depositors eventually were afraid that their savings would be out of reach.

It is worth noting that bank holidays were found to be illegal and it was apparently for that reason Hoover never declared a nationwide holiday himself. Regardless, Roosevelt now has to take action, and he did so by announcing reopenings of the banks. While bank examiners couldn't possibly go through thousands of banks' books, those which were examined were judged to be perfectly safe after rough, superficial analysis that merely reflected the general understanding, shared by savvy depositors. Generally speaking, reopenings were successful not because of Roosevelt confidence speech but because depositors never distrusted their banks in the first place. On the other hand, devaluation fears persisted. Yet people were induced to hold deposits or paper dollars instead of gold for two reasons. First, Roosevelt prohibited gold transactions of any kind. Secondly, the Federal Reserve Board announced that the Fed banks compiled a list of persons who had withdrawn gold, whose names would have been published if they didn't bring the gold back.

1934 Recovery Owing to Gold Inflow

At some point, the economy started to recover, and it was argued that gold inflow fueled that post-1933 recovery. Roosevelt tried to encourage the return flow of gold by regulating gold's market price by just having the RFC purchase it at prices set daily by Roosevelt and his Treasury Secretary. Gold purchase, resulting in a depreciating dollar, would help raise the commodity prices. It appeared however that such de facto devaluation was less effective in bringing gold back to the U.S., to promote money growth, than the de jure devaluation that followed. The reason was because :

with most former gold bloc currencies still fixed to gold, the RFC's gold purchases could only raise gold's market price by depressing other gold bloc nations' price levels. Because the purchases themselves did nothing to raise U.S. prices, the terms of trade stayed unchanged.

What actually caused a rise in commodity prices was the expectation of money growth, because they led traders to expect a dramatic change in the future path of monetary policy.

Nonetheless, it is important to discuss the cause of gold stock growth. The first reason was the devaluation's immediate effect on the dollar value of existing U.S. gold holdings, which rose at once by $2.8 billion (which benefits went straight to the Treasury). The second, most important, reason was the inflow of foreign capital from the start of 1934. Selgin argued that while devaluation stabilized the dollar's gold value, therefore encouraging the return of foreign capital that had taken flight, the situation became precarious in Europe. Hitler became Germany's Fuhrer in 1934. It was the main cause of such a steady stream of capital inflow. Frank Steindl even argued that, if it were not for Hitler threatening european economies, there would be no U.S. recovery until 1941.

Unemployment

But even this recovery was disappointing owing to the persistence of high unemployment. Also, most of the gain in output was due to remarkable post-1933 gains in total factor productivity. Despite huge gold flowing in from Europe, why didn't employment increase as a result ? One reason was the banks' inclination to accumulate excess reserves after the event which occurred during the bank holiday. Selgin shows the following chart :

So, as banks accumulate reserves, as gold reserves grow, the money stock would grow less than proportionately.

Nominal GNP was still growing, nevertheless, remarkably. By 1937 it was 70% above its 1933 level. Employment didn't improve yet since a substantial part of the increase in spending was offset by higher wage rates. Employers gave raises to existing workers instead of hiring more. This looks surprising, as about 20% of the labor force was out of work. And the reason was a simple one :

NRA codes boosted nominal wage rates, and imposed “labor standards” such as overtime premium pay, by regulatory fiat. Both the NIRA and the NLRA promoted formation of labor unions and strengthened workers’ bargaining power over employers. These policies could boost prices, as well as wages, as they gave an extraordinary boost to labor costs of production.

The main reason for adopting such policies is because during the 1920s, the underconsumption theory of depression, bringing the high-wage doctrine with it, became popular. The main idea was that the more people earned money the more they could spend. But in practice the NRA worked differently. It helped the formation of many cartels and would not prevent product prices from rising in response to higher wages. Furthermore, the firms following the NIRA codes tended to hire less labor.

High Wage Fallacy

There is still an argument in favor of the NRA, proposed by Eggertsson, that needs to be discussed. In his papers, he argued that strikes and wage codes (along with New Deal policies such as bank holiday and devaluation) would promote recovery by lowering real interest rates, since the increase in price and wage will boost the expected rate of inflation. But as Selgin explained, this theory rests upon the false premise that any policy that raises the present and expected future level of prices also raises expectations about future income. Indeed, workers have no reason to expect to earn more money if they notice an increase in price levels. Selgin further explains that if the average household becomes more optimistic regarding future (real income) growth rates, this will lead to an increase in the natural interest rate and conversely.

At that time, the Brookings study thoroughly analyzed the NRA, and arrived at the conclusion it failed in many respects. The Brookings stated that raising either the price of labor or goods is not the way to enlarge spending. Raising wage rates relative to the price of goods means the employers were expected to dig into their pockets to finance the wage increases before recouping through higher prices or by reducing workers' hours, which will leave their purchasing power unchanged either way.

The reality was even worse however. The Brookings observes that the prices rise ahead of wages due to anticipation of higher labor costs and they did so even before the NRA codes were operating. And when NRA was operating, it failed to target those in need. NRA wage codes applied only to about half of all workers, and mainly to those who were already highly paid.

By the time NRA was declared unconstitutional, unemployment rate fell from 25% to 18%. But the Brookings report observes we shouldn't credit the NRA for such improvement as its impact was much smaller than what the NRA representatives claimed. The NRA ought to have created 1.75 million more jobs yet it created only 80,000 jobs. But by reducing the total hours worked, the NRA had a negative effect on total output. What the NRA accomplished was dividing a smaller amount of work among more workers. Finally, by increasing living costs, debtors were also made worse off.

Growth in Farm Sector

But the job sector which mattered the most for the New Deal programs was farming, as Roosevelt made it clear with the AAA, an even more important piece of the New Deal than was the NIRA. During the boom, farmers invested heavily in new farmland by arranging mortgage loans with banks, since government policies aimed at boosting farm output.

All of the ingredients leading to a typical ABCT scenario were there. By 1925, mortgage debt rose drastically. After farm product prices collapsed, farm foreclosure rates rose to record levels. Those farm mortgages were the major cause of bank failures during the 20s and the first years of the depression. More banks were to fail owing to rising crop prices which ultimately encouraged the formation of many more lending banks during the period.

The AAA was indeed a measure meant to raise farmers' purchasing power by raising farm product prices. In reality, farmers didn't enjoy those benefits.

To call the AAA's contributions gains to "farmers" is nevertheless misleading, because they mostly ended up going to landlords, rather than to their tenants or to actual farm workers. When AAA benefits went to cash-paying tenants, they tended to be fully offset by higher rents. When, instead, they were meant to be divided between sharecroppers and their landlords, as in the cotton-growing South, the landlords often prevented sharecroppers from being paid directly, while dispensing with those they no longer needed. As a result, hundreds of thousands of tenant farmers and their family members found themselves homeless, with no means of survival save those offered by other New Deal relief programs.

One of the authors of the Brookings' report stated that its contribution to recovery has been minor. Mainly, the increase in both farmers' earnings and their demand for non-farm goods and services was due to other factors, including the Great Plains drought, huge outpourings of public funds other than through the AAA, and the dollar's depreciation.

A more recent study by Hausman also confirmed this point of view. After controlling for the confounding effects of the drought and the AAA, the most important variable was the dollar's devaluation, which caused farm product prices, and traded crop prices especially, to rise both absolutely and relative to the CPI.

Why the 1937 Recession?

While we understand now that the recovery was fueled by gold inflows from Europe but hampered by New Deal measures like NRA and AAA, the industrial production indices fell sharply during 1937, which was known as the Roosevelt recession.

One of the two major causes of the 1937 recession was the decision from the Fed officials to increase banks' minimum reserve requirements (owing to fear of inflation due to gold inflows). But since commercial banks had every reasons to keep some excess reserves (i.e., above the minimum required) as a protection against bank runs after being traumatized by earlier events like the bank holiday, the increase in reserve requirements caused the banks to accumulate even more excess reserves, which ultimately lead to a contraction in credit.

There were some critics to this theory, the main idea of these studies being that such policy didn't lead banks to reduce their lending substantially. Still, other economists made the statement that if such policy didn't immediately reduce credits, it created expectations of actual and future deflation.

The second major cause, one which Friedman and Schwartz considered no less important than the reserve requirements, was the sterilization of gold inflows. This measure was more contractionary than the reserve requirements, thus played a more important role. The growth rate of the monetary base fell from an average annualized rate of 17% between 1934 and 1936 to zero.

Another explanation of the 1937 downturn puts the blame on the cuts in government's spending. This was the claim of Eccles and Currie. According to Currie, the largest single factor in the steady recovery was the excess of Federal expenditures. The problem is that Currie compared government outlays between 1936 and 1937. The veteran's Bonus Act passed in 1936 added so much to government expenditures that such comparison greatly exaggerates the extent of the fiscal stimulus cuts. In fact, from March to September 1937, expenditures were still above the levels of 1934 and 1935. Another, bigger problem is that the decline in expenditures didn't actually caused a decline in income :

As Kenneth Roose, who was then teaching at UCLA, observed in a 1951 article, and as the chart reproduced from it below shows, there's a lag of more than six months between the beginning of the start of the decline in net government spending in December 1936 and the start of the decline in total income, and it wasn't until January 1938 that monthly income fell below its high 1936 average. Yet a large proportion of government spending in the 1930s, including relief payments, became income with no lag at all; and contemporary estimates put the income lag for government payments of all sorts at just one month.

Also, as Selgin noticed earlier, fiscal stimulus didn't contribute much to the 1933-1937 recovery. In this case, stimulus cuts couldn't possibly cause the recession.

That recovery, anyway, was held back by inadequate investment. Between 1931 and 1934, net investment turned negative. Investment in structures showed a slow growth during the recovery period and yet was far below its 1929 level.

Why investments failed to recover as much ? Roosevelt made it crystal clear during his 1932 presidential campaign that the New Deal involved trial and error and it wasn't a coordinated set of policies. As new policies multiplied, the growing uncertainty discouraged long-term investment. The list of such impactful policies is an impressive one:

In 1935, Roosevelt changed his attitude toward rich businessmen with several announcements to the Congress that the concentration of wealth is unfair and very high taxes are required. Roosevelt received a letter from Roy Howard, an influential newspaper editor, who explained that businessmen once gave him support but now they are hostile and threatened.

To illustrate how expectation is important, in 1936 the undistributed profits tax was enacted. Its direct impact wasn't huge but it raised uncertainty about the future, in such a way businesses reduced their desire to invest. Furthermore, a recent study by Roger Farmer using a model including investors' belief shocks found that government spending isn't enough to compensate for the adverse investment shock. Another recent article constructed a policy uncertainty index by counting the number of articles in various newspapers containing the terms "uncertainty" or "uncertain" and "economic" or "economy" together with any of the following : "congress" "legislation," "white house," "regulation," "Federal Reserve," or "deficit." It appears there is a huge increase of that uncertainty index during the 1930s, especially the second half. This latter study is merely suggestive however.

A more direct evidence comes from Sharon Harrison and Mark Weder's time series analysis with VAR. Their variable of interest is what they call a nonfundamental expectation, that is, independent of economic fundamentals such as : the growth rate in real gross national product (y); the growth rate in real money supply, as measured by M2 (m); the rate of change of the GNP deflator (p); and the absolute change in the nominal return on prime commercial paper (cp). They then performed a Granger causality test on output and their measure of nonfundamental confidence, and found that confidence Granger cause output and not vice versa. Overall, their model can explain the decline from 1929 to 1932, the subsequent slow recovery, and the recession that occurred in 1937-1939.

Obviously, given all the evidence, it doesn't follow that business cycles originate purely from confidence or expectation shocks, without any other factor triggering them first, as austrian economics understand well the cause.

Farmer, R. E. (2020). The importance of beliefs in shaping macroeconomic outcomes. Oxford Review of Economic Policy, 36(3), 675-711.

Harrison, S. G., & Weder, M. (2006). Did sunspot forces cause the Great Depression?. Journal of monetary Economics, 53(7), 1327-1339.

Hausman, J. K., Rhode, P. W., & Wieland, J. F. (2019). Recovery from the great depression: The farm channel in spring 1933. American Economic Review, 109(2), 427-72.